Elon Musk just became the world’s first trillionaire after SpaceX went public, marking one of the most remarkable business stories of our time. This deep dive is for entrepreneurs, investors, and anyone curious about how a startup founder built multiple billion-dollar companies and reached unprecedented wealth levels.

Musk’s path from early entrepreneur to trillionaire didn’t happen overnight. We’ll explore his strategic approach to building revolutionary companies across completely different industries – from electric vehicles with Tesla to space exploration through SpaceX. His ability to turn ambitious visions into valuable businesses has created what markets now call the “Elon premium.”

The SpaceX public offering that pushed Musk over the trillion-dollar mark tells a bigger story about investor psychology and risk-taking in today’s markets. We’ll break down why people are betting big on unproven technologies and how Musk’s personal brand drives company valuations beyond traditional financial metrics.

SpaceX IPO raises $75 billion and drives net worth to $1.1 trillion

The pivotal moment that propelled Elon Musk to trillionaire status occurred when SpaceX began trading on the Nasdaq on Friday, June 12, 2026. The initial public offering was priced at $135 per share on Thursday evening, but when trading commenced, shares opened at $150 per share, giving the company a nearly $2 trillion market capitalization. This extraordinary market response boosted Musk’s net worth by $188 billion overnight, from an estimated $982 billion to $1.1 trillion by Friday morning.

Musk’s substantial ownership position in SpaceX proved instrumental in achieving this historic wealth milestone. He owns 4.8 billion shares of SpaceX, valued at $715 billion, along with an additional 350 million stock options worth $50 billion. This gives him a commanding 38% stake in the rocket and AI company, which became the primary driver of his trillionaire status. The $75 billion raised through the IPO not only provided SpaceX with significant capital for expansion but also established the company as one of the most valuable public entities in history.

Tesla’s transformation from startup to world’s most valuable automaker

Before SpaceX’s groundbreaking IPO, Tesla had already established itself as a cornerstone of Musk’s wealth portfolio. The electric vehicle manufacturer contributed approximately $279 billion to Musk’s fortune through his stock holdings and options as CEO. Tesla’s remarkable journey from a startup to becoming a dominant force in the automotive industry laid the crucial foundation for Musk’s eventual path to trillionaire status.

Musk first appeared on Forbes’ World’s Billionaires list in 2012 with an estimated $2 billion fortune, ranking as the 634th-richest person globally. The transformation accelerated dramatically over the subsequent nine years, with Tesla’s soaring stock prices playing a central role. In January 2021, Tesla’s remarkable performance propelled Musk past Jeff Bezos to become the world’s wealthiest person for the first time, demonstrating the company’s critical importance in his wealth accumulation strategy.

Portfolio expansion across space, AI, social media, and transportation sectors

Musk’s strategic diversification across multiple revolutionary industries has created an unprecedented business empire that spans space exploration, artificial intelligence, and transportation. SpaceX, now valued at $2 trillion, represents more than just a rocket company—it’s positioned as both a space exploration and AI enterprise, reflecting Musk’s vision of technological convergence.

During a Forbes Innovator 250 Celebration interview, Musk shared ambitious predictions about the future technological landscape, stating that “in five years, digital intelligence will exceed the sum of all human intelligence” and forecasting “at least 100 million humanoid robots, but maybe a billion” within the same timeframe. He predicted the economy would double in size within five to seven years, emphasizing the transformative potential of his diversified portfolio.

This strategic expansion across sectors has created a combined paper wealth of $1.26 trillion from just his two public companies, Tesla and SpaceX. The portfolio approach has proven remarkably effective, as evidenced by the fact that Musk’s individual wealth now exceeds the combined net worth of the next four richest people globally—Google founders Larry Page and Sergey Brin, Oracle founder Larry Ellison, and Amazon founder Jeff Bezos—whose combined wealth totals $1.09 trillion.

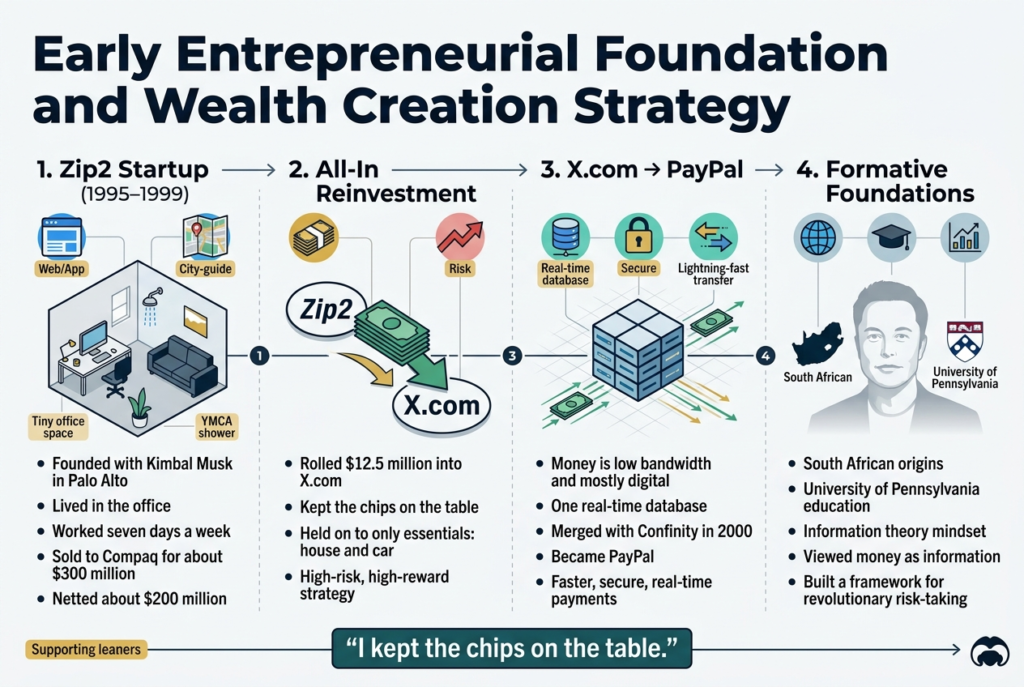

Initial fortune from Zip2 and PayPal sales netting $200 million

Musk’s journey to becoming the world’s first trillionaire began with his extraordinary entrepreneurial foundation built through two groundbreaking ventures in the late 1990s. The genesis of his wealth creation strategy started with Zip2, a web software startup that created online city guides for newspapers. Founded alongside his younger brother Kimbal Musk in Palo Alto, California in 1995, this venture exemplified the bootstrap mentality that would define Musk’s approach to business.

The early days of Zip2 revealed Musk’s unwavering commitment to his vision. Rather than securing traditional accommodations, the brothers rented a small office space where they literally lived, sleeping on a couch and showering at the local YMCA. This extreme frugality wasn’t born of choice but necessity—they were “so hard-up that we only had one computer,” as Musk later recounted. The operational structure required the website to function during business hours while Musk coded throughout the night, working seven days a week in a relentless pursuit of perfection.

This dedication paid off spectacularly when Compaq acquired Zip2 for approximately $300 million in 1999. However, Musk’s experience with Zip2 left him with a sense of unfulfilled potential, describing the situation as “frustrating” because “we built incredible technology at Zip2, and it had not been used.” This dissatisfaction with being constrained by customers motivated his next venture.

Strategic reinvestment into high-risk, high-reward ventures

With his Zip2 windfall, Musk demonstrated the high-risk, high-reward investment philosophy that would become his trademark. Rather than diversifying his wealth or securing safer investments, he made the audacious decision to roll most of his Zip2 earnings into his next venture, X.com, investing $12.5 million of his own money. This represented nearly everything he had earned from the Zip2 sale, keeping only essential personal assets like his house and car.

Musk’s approach to X.com was rooted in his deep understanding of information theory and financial systems. He identified that “money is low bandwidth and mostly digital” and recognized the inefficiencies in 1990s financial infrastructure, which he characterized as “a bunch of ancient mainframes, running ancient code, doing batch processing with poor security, and a series of heterogeneous databases. A herky-jerky frickin’ monstrosity.”

His vision for X.com was revolutionary—creating a real-time, secure, and fast financial system that would function as “just one real-time database.” This theoretical framework led to what would eventually become PayPal after X.com merged with Confinity in 2000. The strategic insight was to improve the bandwidth and reduce latency of money movement, eliminating the inefficiencies of mailing checks and waiting for bank clearances.

When Sequoia Capital invested $5 million in X.com in 1999, with Mike Moritz joining the board, Moritz advised Musk against investing virtually everything in his startup. However, Musk’s response was characteristic: “I kept the chips on the table.” This all-in mentality reflected his belief that revolutionary changes required revolutionary commitment.

University of Pennsylvania education and South African origins

While the reference content doesn’t provide extensive details about Musk’s educational background or South African origins, it’s clear that his formative experiences shaped his approach to entrepreneurship and wealth creation. The mention of his University of Pennsylvania education in the blog outline suggests this foundation contributed to his theoretical understanding of complex systems, particularly evident in his sophisticated analysis of financial infrastructure through information theory principles.

His ability to conceptualize money as “information” and “a database for resource allocation across time and space” demonstrates the analytical framework he developed, likely during his academic years. This theoretical foundation enabled him to identify inefficiencies in existing systems and envision revolutionary solutions that others might overlook.

The combination of his international perspective from South African origins and American higher education created a unique lens through which he viewed business opportunities, setting the stage for his unprecedented approach to wealth creation and strategic risk-taking.

SpaceX’s dominance in rockets, satellites, and space exploration

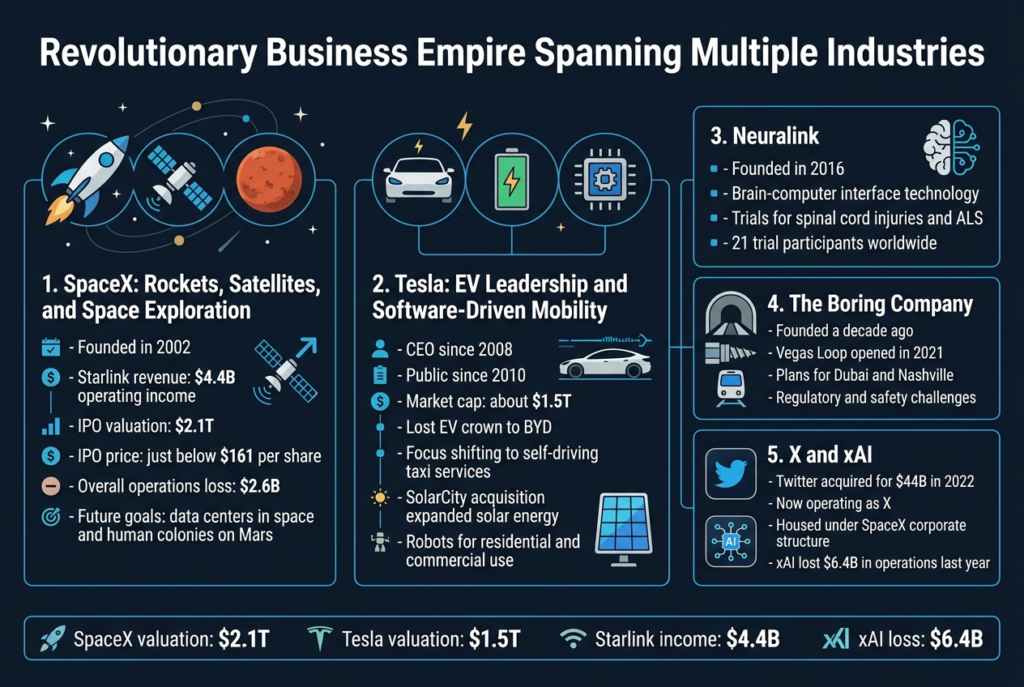

Now that we have covered Musk’s path to trillionaire status, we can examine the revolutionary business empire he has built across multiple industries. SpaceX stands as the cornerstone of this empire, having evolved far beyond its original rocket manufacturing focus since Musk founded it in 2002. The company has achieved unprecedented dominance in space exploration through its integrated approach to aerospace technology and satellite communications.

The satellite communications service Starlink represents SpaceX’s most lucrative revenue stream, generating an impressive $4.4 billion in operating income last year alone. This cash-generating capability has provided the financial foundation for SpaceX’s ambitious expansion plans, including lofty goals ranging from putting data centers in space to establishing human colonies on Mars.

Following its historic initial public offering on Friday, SpaceX debuted with the largest IPO in history, closing at just below $161 per share and achieving a total market valuation of $2.1 trillion. This remarkable market response demonstrates investor confidence in the company’s multiplanetary vision, despite the fact that SpaceX lost $2.6 billion overall from operations last year.

The company has also expanded its portfolio through strategic acquisitions, housing social media platform X (formerly Twitter) under its umbrella after Musk’s $44 billion acquisition in 2022. Additionally, SpaceX merged with Musk’s artificial intelligence company xAI earlier this year, positioning itself as a leader in AI development alongside its aerospace operations.

Tesla’s electric vehicle leadership and software-driven innovation

Previously, I’ve discussed SpaceX’s dominance in aerospace, but Tesla represents another pillar of Musk’s revolutionary business empire. As CEO since 2008, Musk has transformed Tesla from a startup into a trillion-dollar company that went public in 2010 and joined the prestigious S&P 500 trillion-dollar club. The company currently maintains a market capitalization of approximately $1.5 trillion.

Tesla’s leadership position in the electric vehicle market, however, has faced significant challenges. The company lost its crown as the world’s largest EV maker to China’s BYD last year, highlighting the intensifying competition in the electric vehicle space. Sales were further impacted by boycotts related to Musk’s political positions, though these numbers have since shown some recovery.

Musk has consistently emphasized that Tesla’s future lies not primarily in traditional car sales but in revolutionary transportation solutions, particularly self-driving taxi services. This software-driven innovation approach represents a fundamental shift from manufacturing to mobility services.

Beyond automotive applications, Tesla has diversified into multiple sectors through strategic acquisitions and internal development. The company acquired SolarCity, founded by Musk and his cousins, expanding into solar energy business operations for nearly a decade. Tesla has also increased production of robots designed for both residential and commercial applications, demonstrating its commitment to automation technology across various industries.

Diverse ventures including Neuralink, The Boring Company, and Twitter acquisition

With this in mind, next, we’ll examine Musk’s diverse portfolio of innovative ventures that extend beyond his flagship companies. Neuralink, co-founded by Musk in 2016, represents his ambitious entry into brain-computer interface technology. As CEO of this groundbreaking company, Musk has positioned Neuralink among the leading groups working to connect the human nervous system directly to machines.

The company has made significant progress in clinical applications, launching trials for individuals with spinal cord injuries, ALS, and other neurological conditions. Neuralink has announced multiple successful brain implant procedures in recent years, with the company reporting 21 trial participants worldwide as of January. This medical technology venture demonstrates Musk’s commitment to solving complex human health challenges through innovative technological solutions.

The Boring Company, another Musk-founded venture established a decade ago, focuses on tunnel digging and underground transportation systems. The company’s most notable achievement is the “Vegas Loop,” a network of underground tunnels utilizing Tesla vehicles that first opened around the Las Vegas Convention Center in 2021. Despite ambitious plans for high-speed transit networks in Dubai and Nashville, the company has encountered significant regulatory challenges, including accusations of breaking multiple safety and environmental requirements in Las Vegas, where the full route remains unfinished.

The Twitter acquisition, completed for $44 billion in 2022, represents one of Musk’s most controversial business moves. Now operating as platform X and housed under SpaceX’s corporate structure, the social media company has struggled financially, with both X and the associated xAI artificial intelligence business posting substantial losses—xAI alone lost $6.4 billion in operations last year.

Record-breaking $75 billion IPO surpassing Saudi Aramco’s previous record

SpaceX has officially rewritten the IPO record books with an unprecedented $75 billion public offering that dwarfs all previous market debuts. The company successfully sold more than 555 million shares at $135 each, generating a funding haul that more than doubles Saudi Aramco’s previous record of $29.4 billion set in 2019. This historic offering represents not just a milestone for SpaceX, but a seismic shift in how investors value space technology and infrastructure companies.

The scale of this IPO becomes even more remarkable when viewed in the broader context of 2026’s public offering landscape. SpaceX’s single $75 billion raise exceeds the combined $36 billion raised by 71 other IPOs throughout the year, demonstrating the extraordinary investor appetite for Musk’s space venture. The offering experienced unprecedented demand, with the book running approximately five times oversubscribed, forcing the company to allocate shares selectively among eager institutional investors.

First-day trading surge of 19% despite company losses

With this record-breaking IPO now behind us, the market’s immediate response proved equally dramatic. SpaceX shares opened trading at the $135 IPO price but quickly surged as demand continued to outstrip supply. By midday on June 12, the stock was trading at $152.66, representing a substantial 13% gain from the opening price and demonstrating robust investor confidence despite the company’s current unprofitability.

This first-day performance is particularly noteworthy given the competitive allocation process that left many investors scrambling for shares. Retail investors faced significant constraints, receiving allocations in the low-20% range—well below the approximately 30% allocation SpaceX had originally targeted for individual investors. Institutional heavyweight BlackRock alone sought at least $5 billion worth of shares, illustrating the institutional demand that drove the oversubscription and subsequent trading premium.

$2.1 trillion market valuation making it sixth largest U.S. public company

Now that we have covered the immediate market mechanics, the resulting valuation places SpaceX among America’s corporate giants. The company’s market debut established a valuation of nearly $1.8 trillion, instantly positioning it as the seventh most valuable U.S. company and remarkably surpassing Tesla’s $1.49 trillion market capitalization.

This valuation milestone carries profound implications beyond SpaceX itself, as it pushes founder Elon Musk to the precipice of becoming the world’s first trillionaire. The timing proves particularly significant given Tesla’s challenging performance, with shares down 11.24% year-to-date through June 11, making SpaceX’s success crucial to Musk’s wealth trajectory.

The interconnection between Musk’s companies adds another layer of complexity to this valuation story. Tesla disclosed a substantial $2 billion equity investment in SpaceX along with a semiconductor fabrication partnership at Gigafactory Texas, providing Tesla shareholders with direct exposure to SpaceX’s public market success. This strategic alignment between the companies creates a unique dynamic where success in one venture directly benefits stakeholders in the other, amplifying the overall impact of SpaceX’s remarkable public market debut.

$8.7 billion in losses between 2025 and March 2026

Despite the extraordinary hype surrounding SpaceX’s upcoming IPO, the company’s financial reality presents significant challenges that investors must carefully consider. The company recorded a staggering net loss of $4.95 billion in 2025 alone, primarily driven by heavy AI-related expenditures following the merger with xAI. This massive loss occurred on revenue of $18.7 billion, highlighting the company’s struggle to achieve profitability despite its dominant market position.

The integration of xAI assets, including the LLM Grok, the X social media platform, and the massive Colossus data center operation, has fundamentally altered SpaceX’s financial profile. Over the past five quarters, the company has invested at least $20 billion in building up Grok and establishing its Memphis-based Colossus data center, with the company’s prospectus indicating that AI-related investments are set to grow further without guarantee of solid returns.

The AI pivot has transformed SpaceX from a relatively cleaner operating story focused on launch services and Starlink into a much heavier investment profile with substantial cash burn. While Starlink provides recurring revenue and the launch business maintains strategic advantages, the AI segment continues to drain resources significantly. This financial pressure is particularly concerning given that Grok has not demonstrated significant performance advantages over leading AI peers, preventing it from gaining meaningful market share despite the massive capital investment.

Unproven technologies and ambitious timelines for Mars colonization

Now that we’ve examined the immediate financial challenges, the technological uncertainties surrounding SpaceX’s most ambitious projects present additional layers of investment risk. The company’s valuation appears to heavily depend on the successful development and deployment of unproven technologies, particularly the next-generation Starship V3 and Mars colonization initiatives.

While SpaceX’s current Starship program holds promise for expanding payload capacity from 35 metric tons to 100 metric tons, the technology remains largely experimental. The success of Starship is critical not only for Mars ambitions but also for enabling other futuristic projects like orbital data centers, which Musk claims will help meet insatiable AI demand. However, these orbital data centers represent another longshot project with uncertain economics and unproven technological feasibility.

The Mars colonization timeline presents perhaps the most speculative element of SpaceX’s current valuation. Investors are essentially paying for optionality on interplanetary infrastructure development, despite the numerous technical, regulatory, and logistical challenges that remain unresolved. The company’s prospectus reportedly frames access to a $28.5 trillion total addressable market, with Mars-related opportunities forming a significant portion of this calculation. However, this represents a vision trade where investors are buying the right to participate in markets that either don’t exist yet or have no proven economics at scale.

Analyst concerns about significant overvaluation at current prices

With these technological and financial uncertainties in mind, leading analysts have expressed serious concerns about SpaceX’s proposed IPO valuation. Morningstar analyst Nicholas Owens has directly challenged the company’s $1.75 trillion target valuation, arguing that SpaceX’s actual value is approximately $780 billion—about 55% below the IPO target.

Owens labeled SpaceX shares as “overvalued in almost any scenario, at least in the near term,” despite acknowledging the company’s strong launch business and growing Starlink operation. The valuation concerns stem from the disconnect between current operating performance and future expectations. By revenue, SpaceX would rank as only the 200th biggest company in the U.S., yet the proposed valuation would make it the seventh-biggest company overall.

The overvaluation concerns are compounded by several market dynamics that may artificially inflate the stock price post-IPO. These include outsized interest from underwriting investment banks, a limited float of only 3% of shares offered to public investors, and automatic inclusion in the Nasdaq 100 that will force index funds to purchase shares. Smart investors may be better positioned to wait for more favorable entry points when early shareholders begin selling their holdings through SpaceX’s novel lockup structure, which allows staged selling beginning just weeks after the IPO rather than the traditional 180-day restriction period.

The fundamental challenge lies in the gap between SpaceX’s undeniable technological achievements and the premium investors are being asked to pay for future potential. While the company maintains narrow moats in launch economics and satellite-based connectivity, analysts warn that competitive pressures from Blue Origin, Rocket Lab, and Chinese startups could erode these advantages over time, making the current premium valuation difficult to justify.

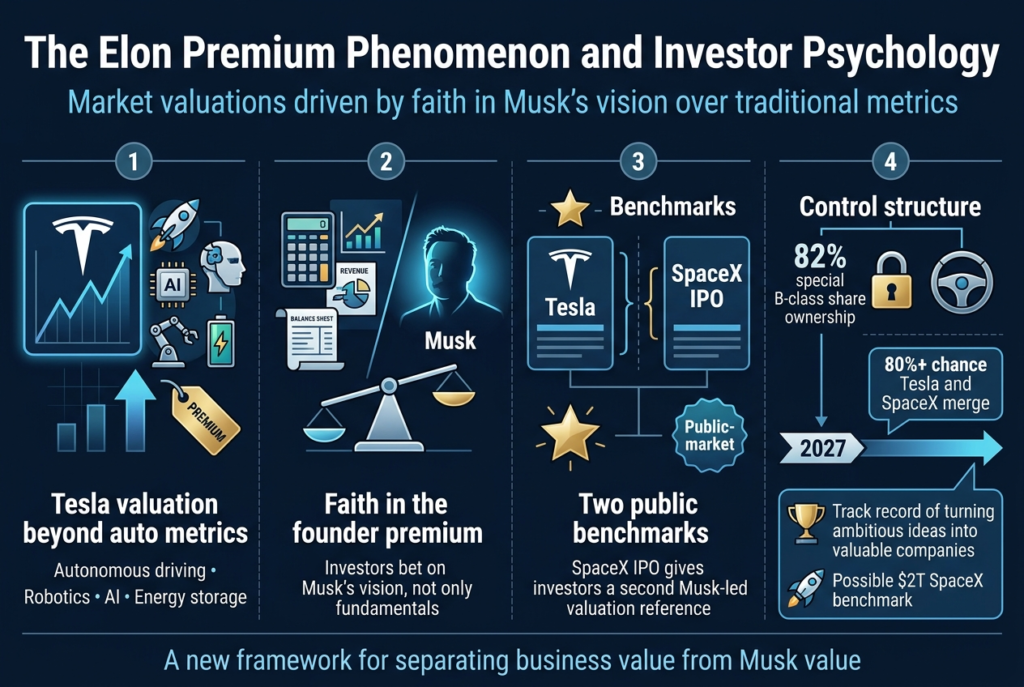

Market valuations driven by faith in Musk’s vision over traditional metrics

For years, Tesla Inc. investors have grappled with a fundamental question that has never had a clear answer: How much of Tesla’s valuation belongs to Elon Musk himself? This debate has become increasingly critical as Tesla’s market value has grown far beyond what traditional automotive metrics would suggest. Bulls argue the company deserves a premium because it sits at the center of multiple disruptive technologies, from autonomous driving and robotics to artificial intelligence and energy storage.

Bears have long countered that part of Tesla’s valuation reflects something less tangible: the market’s willingness to bet on Musk himself rather than purely on business fundamentals. This phenomenon represents a departure from traditional investment analysis, where valuations are typically anchored to concrete financial metrics and industry benchmarks.

The expected SpaceX IPO is generating excitement because it would give public investors access to one of the world’s most valuable private companies. However, the bigger implication may be what it reveals about Tesla and the broader “Musk premium” phenomenon. For more than a decade, Tesla has effectively been the default way for many investors to gain exposure to Musk’s vision of the future, as SpaceX remained private.

Concentrated control through 82% special B-class share ownership

Now that we have covered the market’s faith-based approach to valuation, the concentrated ownership structure becomes a critical factor in understanding investor psychology. This dynamic changes significantly once SpaceX begins trading publicly, as investors will suddenly have two separate data points for valuing Musk-led innovation.

The timing is particularly interesting because Wedbush analyst Dan Ives recently said he sees an “80%+” chance that Tesla and SpaceX ultimately merge by 2027. Whether that prediction proves correct may be less important than the valuation debate it has already sparked. This concentrated control structure allows Musk to maintain strategic direction across his ventures while creating a unique investment dynamic where traditional governance models take a backseat to visionary leadership.

Track record of turning ambitious ideas into valuable companies

With this ownership concentration in mind, Musk’s track record becomes the foundation for investor confidence. If SpaceX commands the kind of valuation some investors expect, potentially approaching $2 trillion over time, Wall Street will gain a powerful benchmark for assessing how much value investors assign to Musk’s leadership, vision and execution capabilities.

In other words, the market may finally be able to separate the value of Tesla’s businesses from the value of being associated with Musk. This new valuation framework has implications that extend far beyond Tesla, potentially reshaping how investors evaluate founder-led companies and the premium they’re willing to pay for visionary leadership. The arrival of a second publicly traded Musk stock creates an unprecedented opportunity to quantify what has long been an intangible but significant factor in modern investing.

Legal battles over Tesla CEO pay package and shareholder concerns

Elon Musk’s protracted legal saga over his $56 billion Tesla compensation package continues to cast a long shadow over the electric vehicle giant. Despite a recent shareholder vote overwhelmingly ratifying the 2018 pay deal and approving a move of Tesla’s legal domicile to Texas from Delaware, the battle is far from over. The company now faces the formidable task of convincing a skeptical Delaware Court of Chancery judge, Kathaleen McCormick, to reverse her earlier decision that voided the package.

Judge McCormick had previously rescinded the pay package in January, citing that Musk improperly controlled the 2018 board process and that investors weren’t fully informed. While Tesla argues the recent shareholder vote, conducted with extensive disclosures including McCormick’s 200-page ruling, effectively corrected these issues, legal experts remain cautious. Brian Quinn, a professor at Boston College Law School, emphasizes that the court will demand proof the vote was uncoerced and not influenced by Musk.

The stakes are incredibly high for Tesla, currently trading at $355.28, down 1.81% today, with a market cap of $1.33 trillion. The uncertainty surrounding Musk’s compensation could impact investor confidence, particularly as the company navigates slowing sales and increased competition. Some major shareholders and even smaller investors voted against the package, citing its sheer size and Musk’s growing list of distractions across his various ventures.

Adding another layer of complexity, at least one shareholder, Donald Ball, has already filed a legal challenge to the ratification vote, accusing Musk of “strong-arm, coercive tactics.” Ball’s lawsuit points to Musk’s public statements on X, where he indicated discomfort transforming Tesla into an AI leader without 25% of the company’s stock.

Political involvement and Trump administration role creating market volatility

Now that we have examined the legal complexities, the intersection of Musk’s political activities with his business empire presents equally significant challenges. Tesla’s once-unrivaled brand loyalty has reportedly plummeted, a concerning trend largely attributed to CEO Elon Musk’s increasingly visible political alignments and inflammatory public statements, particularly his endorsement of President Donald Trump. Data from S&P Global Mobility indicates that Tesla has seen its loyalty fall to industry-average levels, representing an “unprecedented” decline according to S&P analyst Tom Libby.

The impact of Musk’s political activities is significant, especially among Tesla’s traditionally eco-conscious customer base. A 2024 Pew Research Center poll revealed that Democrats are three times more likely to buy an EV than Republicans, highlighting the partisan divide. Tesla’s “net favorability rating” sank to 3% for the week ended January 28, compared to 9% in January 2024, and a robust 33% in January 2018.

These controversies are translating into tangible business challenges. Tesla reported its first annual sales decline in 12 years in 2024, with sales falling 1% from the prior year, even as global EV sales rose 7.3%. Protests have erupted at Tesla dealerships across the U.S. over Musk’s proximity to the Trump administration. Analysts like Wedbush Securities’ Dan Ives have noted a 17% drop in the carmaker’s stock since Trump’s January 20 inauguration, attributing it to the “visible perceived downside impact” of Musk’s White House involvement.

Musk’s public spat with President Trump sent shockwaves through major U.S. stock indices, with the S&P 500 declining by 0.5%, the Dow Jones by 0.3%, and the Nasdaq Composite by 0.8%. Tesla’s market capitalization took a staggering $152 billion hit in mere hours during the Trump-Musk feud, underscoring the market’s sensitivity to personality-driven narratives.

Conflicts of interest and risks of single-person dependency

With this political volatility in mind, the broader implications of Tesla’s dependence on a single individual become increasingly apparent. The inextricable link between Musk’s personality and Tesla’s brand presents both opportunities and risks that extend far beyond immediate market fluctuations. His past run-ins with regulators, such as the 2018 SEC charge for misleading investors with his “funding secured” tweet about taking Tesla private, serve as a stark reminder of the legal consequences of his social media activity. Both Musk and Tesla were fined $20 million each in that episode.

The long-term risks associated with Musk’s controversies are substantial. If government contracts for Tesla or SpaceX are jeopardized, it could curb innovation in vital U.S. sectors. The company’s reliance on a single individual, coupled with declining brand loyalty and sales headwinds, introduces significant volatility. Some major shareholders have expressed concerns about Musk’s growing list of distractions across his various ventures in rockets, AI, social media, neuroscience, and tunnel digging, highlighting broader concerns about the CEO’s focus and the company’s future direction.

The $258 billion Dogecoin lawsuit, accusing Musk of running a pyramid scheme, remains active as of February 2026, testing how the law treats influencer-driven markets. This ongoing litigation could shape future communication standards and regulatory frameworks, demonstrating how Musk’s influence extends beyond Tesla into the broader financial ecosystem. For investors, navigating this landscape requires acknowledging both the disruptive potential and inherent risks of such concentrated dependency on a single, highly controversial figure.

Mars Colonization and Multi-Planetary Life Expansion Goals

Now that we have covered the current market dynamics, Musk’s most ambitious revenue diversification strategy centers on his long-standing Mars colonization plans, which trace back to his 2001 involvement with the Mars Society. Having joined their board and donated $100,000, Musk’s initial vision for “Mars Oasis” – an automated greenhouse on Mars – has evolved into a comprehensive multi-planetary expansion strategy that could revolutionize humanity’s economic footprint beyond Earth.

SpaceX’s Mars colonization architecture relies on the fully reusable Starship system, featuring a Super Heavy booster and Starship spacecraft constructed from stainless steel and powered by Raptor engines. The vehicle design incorporates methane fuel production capabilities through the Sabatier process, enabling on-Mars fuel generation for return journeys. This technological foundation supports Musk’s ambitious timeline of establishing a self-sustaining colony by 2050, with initial crewed missions potentially beginning no earlier than 2029.

The economic model for Mars colonization targets dramatic cost reduction, aiming to decrease transportation costs from an initial $10 million per person to eventually $100,000 per person. SpaceX plans to transport one million people to Mars using 1,000 Starships during biennial launch windows, with each journey lasting 80-150 days. The first crewed mission would involve approximately 12 people focused on building propellant plants and establishing rudimentary infrastructure, with rapid colonist increase following successful initial landings.

Critical to the colony’s economic viability is in situ resource utilization, harvesting CO2 from Mars’ atmosphere to produce fuel, breathable air, and other essential resources. The plan envisions achieving self-sufficiency within seven to nine years through local resource exploitation including water ice, oxygen, and methane production for both life support and fuel systems.

Orbital Data Centers and Space-Based Infrastructure Development

Previously, I’ve examined how Musk’s terrestrial ventures have disrupted traditional industries, but his space-based infrastructure ambitions represent an entirely new frontier for revenue generation. While the reference content primarily focuses on Mars colonization efforts, the underlying Starship technology and space infrastructure capabilities position SpaceX to develop orbital facilities that could serve multiple commercial purposes.

The Super Heavy booster and Starship system’s reusable architecture creates unprecedented payload capacity for establishing permanent space-based infrastructure. With journeys to Mars averaging 115 days and the capability to transport massive cargo loads, the same technological foundation supports the development of orbital installations that could serve as data processing centers, manufacturing facilities, and communication hubs.

The methane fuel production technology developed for Mars missions, utilizing the Sabatier process, demonstrates SpaceX’s capability to create self-sustaining orbital operations. This technological expertise in closed-loop resource utilization could enable permanent orbital installations that generate revenue through space-based services while reducing dependency on Earth-based infrastructure.

AI Competition with Anthropic and OpenAI Through xAI Venture

With this in mind, next, we’ll examine how Musk’s AI ambitions through xAI represent a strategic diversification beyond aerospace and automotive sectors. While the reference content doesn’t provide specific details about xAI’s competitive positioning against Anthropic and OpenAI, the Mars colonization plans reveal significant AI integration requirements that could drive xAI’s development trajectory.

The complexity of managing a self-sustaining Mars colony involving one million colonists, automated resource processing, and life support systems necessitates advanced AI capabilities. The seven-to-nine-year timeline for achieving colony self-sufficiency requires sophisticated automation for CO2 processing, oxygen production, methane synthesis, and habitat management. These technical requirements position xAI development within the broader context of Musk’s multi-planetary expansion strategy, creating synergies between AI advancement and space colonization goals.

The automated systems required for Mars resource utilization, including the proposed propellant plants and atmospheric processing facilities, represent real-world testing environments for AI technologies that could later compete in terrestrial markets against established players like Anthropic and OpenAI.

Elon Musk’s ascent to becoming the world’s first trillionaire represents more than just unprecedented wealth accumulation—it exemplifies the power of visionary entrepreneurship and strategic diversification across revolutionary industries. From his early ventures with Zip2 and PayPal to building Tesla into the world’s most valuable automaker and SpaceX into a $2.1 trillion space enterprise, Musk has consistently defied conventional wisdom and market skepticism. His journey demonstrates how ambitious goals, from making electric vehicles mainstream to establishing colonies on Mars, can translate into extraordinary market valuations when backed by technological innovation and unwavering execution.

The “Elon Premium” phenomenon surrounding Musk’s companies reflects both the opportunities and risks inherent in betting on transformational technologies. While critics point to governance concerns, cash burn rates, and unproven business models, investors continue to reward Musk’s track record of turning seemingly impossible ideas into reality. As SpaceX joins Tesla in the public markets and Musk’s influence spans automotive, space, AI, and social media, his empire serves as a compelling case study for how singular vision and relentless innovation can reshape entire industries. For investors and entrepreneurs alike, Musk’s rise offers valuable lessons about the potential rewards of thinking beyond traditional boundaries—while highlighting the importance of understanding the substantial risks that come with revolutionary ambitions.